In the last 10 years, CFO Strategies has helped companies obtain lines of credit totaling over $100 million and we recently helped several clients obtain new banking relationships and obtain over $10 million of new credit lines during the COVID-19 pandemic.

Companies need lines of credit to finance business operations (working capital), especially newer companies, seasonal companies, and companies with inconsistent cash flows. Many small-to-midsize companies do not have a strong internal finance and accounting staff and struggle to provide the financial information necessary to obtain financing or to ensure compliance with loan terms.

In addition, many companies may need lending but might not know how to get it or what types of information they will need to provide to a bank or other lending institution.

Let’s say that your company needs working capital to cover operating needs or for expansion. Or, you are an entrepreneur with a great business idea and you need the cash to build your business. No one needs to tell you how difficult it is to get financing these days, yet it is possible to get the cash you need with some diligence. Banks are lending. The key is to know what the lenders look for and to ensure that their needs are met, so yours can also be met.

We are in a world where it feels like to get a loan you first have to prove that you don’t need one. Yet, lenders will lend – it’s what they do – but they need to have the confidence that the business can pay back the loan and do so timely. You have to give them that confidence. One good way to meet the lenders’ needs and get the financing you desire is to look at your company and its financial picture in the same way that the lender does. If you can put yourself in the lender’s shoes and objectively conclude that all the loan payments will be made on time and according to the loan’s terms, then you will raise the likelihood of getting the financing and with more favorable terms – even in this market.

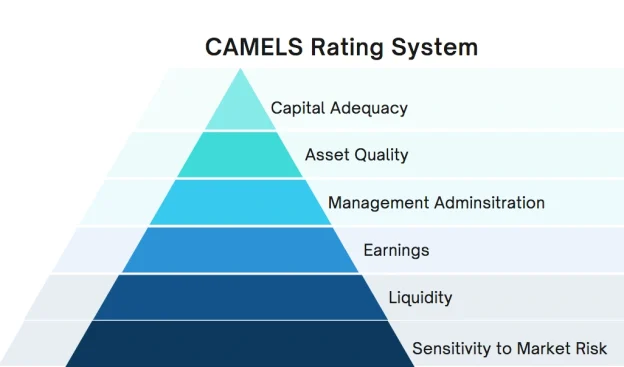

Banks are highly regulated companies and they are periodically examined using a rating system known as CAMELS to determine how safe and sound the bank is. The CAMELS rating impacts the amount of capital a bank is required to carry which impacts the extent to which banks may lend. Banks will look at their customers and prospective borrowers using the same criteria that they are subject to when under examination. Therefore, every borrower should be aware of the CAMELS system in order to be sure that their company meets the minimum standards that banks consider in assessing the borrower and related loan quality. Meeting those standards will raise the likelihood that the loan is funded with the most favorable terms possible.

The CAMELS rating system evaluates the bank’s overall condition and performance by assessing the following six components:

Capital is the amount available after all assets and liabilities are settled, but it is also the safety net available to cover problems, risks, and growth. Each company should maintain an amount of capital commensurate with the overall financial condition of the company and which enables management to address emerging business risks and operational needs. Capital adequacy considers the nature, trend, and volume of problem assets and the adequacy loss reserves for potentially uncollectible receivables. Capital adequacy also includes a company’s access to capital markets and other sources of capital, as well as plans and prospects for future growth and past experience in managing growth.

The borrower needs to demonstrate to the lender that capital is adequate to cover existing business risks, unanticipated but possible adverse events, and planned growth.

Asset quality reflects the quantity of existing and potential credit risk associated with assets such as receivables, investments, property, and other assets that would need to be converted to cash to meet obligations. Asset quality includes off-balance-sheet transactions as well as unfunded commitments and standby letters of credit. Also factored are other risks that may affect the value or marketability of a company’s assets, including, but not limited to, operating, market, reputation, strategic, and compliance risks.

The borrower needs to demonstrate to the lender that asset values on the books are recoverable at least at the amounts stated, that there is no unrecorded impairment, and that working capital and current ratios are adequate. Current assets should be adequate to cover all short term obligations.

A company’s board of directors does not need to be actively involved in day-to-day activities, however, they must provide clear guidance regarding acceptable risk exposure levels and ensure that appropriate policies, procedures, and practices have been established. Senior management is responsible for developing and implementing policies, procedures, and practices that translate the board’s goals, objectives, and risk limits into prudent operating standards.

The evaluation of management deals with the oversight and support of all company activities by the board of directors and management. The evaluation includes the ability of the board and management, in their respective roles, to plan for and respond to risks that arise from changing business conditions or the initiation of new activities or products. The evaluation will also consider the accuracy, timeliness, and effectiveness of management information and risk monitoring systems and whether they are appropriate for the company’s size, complexity, and risk profile. Audit results and compliance with laws and regulations are also a factor.

The borrower needs to build credibility with the lender. Credibility is built by demonstrating in-depth knowledge of the business, clearly articulating the business plan and results, showing how management deals with risk and changing circumstances, and by responding to the underwriter’s questions timely.

The evaluation of earnings considers the quantity and trend of earnings, as well as the quality of earnings. The quantity and quality of earnings can be affected by excessive or inadequately managed risks that may result in losses or require additional reserves, or by high levels of market risk that may unduly expose a company’s earnings to volatility. The quality of earnings may also be diminished by undue reliance on extraordinary gains and nonrecurring events, including tax effects. Future earnings may be adversely affected by an inability to forecast or control funding and operating expenses, improperly executed or ill-advised business strategies, or poorly managed or uncontrolled exposure to other risks.

The borrower needs to demonstrate to the lender positive trends in “core” earnings The quality and source of earnings need to be strong (e.g. with reputable customers and in strong markets) and the level of expenses in relation to operations must be controlled and be comparable to industry standards. Management will need to demonstrate adequate budgeting systems, reliable forecasting processes, and effective management information systems.

The adequacy of a company’s liquidity is evaluated. Consideration is given to the current level and prospective sources of liquidity compared to funding needs, as well as to the adequacy of funds management practices. Funds management practices should ensure that the company is able to maintain a level of liquidity sufficient to meet its financial obligations in a timely manner. In addition, funds management practices should reflect the company’s ability to manage unplanned changes in funding sources, as well as respond to changes in market conditions that affect the ability to quickly liquidate assets with minimal loss. Liquidity should not be maintained at a high cost or through undue reliance on funding sources that may not be available in times of financial stress or adverse changes in market conditions.

The borrower needs to demonstrate to the lender that timely and effective cash management procedures are in place. The borrower should provide the lender with cash flow forecasts to show anticipated cash balances and demonstrate the ability to satisfy its obligations as well as the debt service from the loan being requested. The lender will want to see that receivables have been collected on a timely basis, aged receivables are actively managed and are at reasonable levels, and liabilities are paid according to contractual terms.

The sensitivity to market risk component reflects the degree to which changes in interest rates, foreign exchange rates, commodity or material prices, or equity prices can adversely affect a company’s earnings or economic capital. Consideration should be given to management’s ability to identify, measure, monitor, and control market risk. The company’s size, the nature and complexity of its activities, and the adequacy of its capital and earnings in relation to its level of market risk exposure are factors.

The borrower needs to demonstrate to the lender that it has appropriate procedures in place to control market risk. In financial institutions, this may include asset-liability gap management. In commercial companies, it may include practices to lock in prices or hedge against changes in prices (e.g. purchasing forward commitment contracts to hedge against rising fuel costs where fuel is a significant cost). The quality of management (as discussed above) is a key interrelated factor in evaluating how the company manages market risk.

Other lenders such as non-regulated finance companies, leasing companies, credit unions, and mortgage banks are not subject to the CAMEL ratings or regulations. However, it would be prudent to consider the same criteria in order to meet today’s high lending standards. The current lending environment is difficult for sure. Cash is not flowing as freely as it did a few years ago. Yet, financing is available to companies with good business plans and strong management oversight that deliver results. Thinking like your banker and proactively providing the information described above will go a long way toward not only getting the financing you need but with the best possible terms.

CFO Strategies works with companies that have existing lines of credits and term loans, as well as companies that are looking for new banking relationships. Our seasoned professionals have established banking relationships and we are able to help companies build new banking relationships and obtain loans and lines of credit. In addition, we provide financial reporting to banks to help obtain financing as well as to maintain such financing through reporting that demonstrates compliance with debt covenants. Contact us today to learn more.